米議会で進んでいる2兆円規模の予算内で、一番重要なポイントは最大4.5兆ドルもの社債や州・地方債への信用供給ではないかと考えている。ものすごく簡単にいうと4.5兆ドルほどFRBが買い取りますよんという話だ。既に4.7兆円ほどの資産買入をしているFRBは、資産を倍増して9兆円を超える資産になる可能性がある。

東海岸時間の明日26日朝7時からパウエル議長による会見を行う予定。

米議会で審議中の大規模な新型コロナウイルス景気対策法案が成立すれば、連邦準備制度理事会(FRB)が信用フローの維持と米企業への直接融資に使うことができる額は最大4兆5000億ドル(約500兆円)に上る可能性がある。(中略)

https://www.bloomberg.co.jp/news/articles/2020-03-26/Q7RTAOT0AFB601?srnd=cojp-v2

FRBは財務省と連携しこの資金を信用リスクに対するバックストップに活用し、社債や短期の州・地方債の市場を支えるほか、大企業や中規模企業への直接融資も行う。

尚、社債なら何でもかんでも買うというわけではなく、 投資適格級(S&P社の格付ではAAA〜BBBまでをinvestment grade) の米国企業のみで、投資適格級社債に基づくETFも購入すると考えられている。

The purchasing of corporate bonds by the Federal Reserve will focus on debt issued by investment grade U.S. companies and U.S.-listed exchange-traded funds that provide broad exposure to the market for U.S. investment grade corporate bonds.

https://www.forbes.com/sites/nathanvardi/2020/03/23/the-federal-reserve-moves-to-buy-corporate-debt/#55928db54c47

金額の規模だけみると大きいのだが、果たしてこの規模で足りるのかどうかを少し考えてみようと思う。

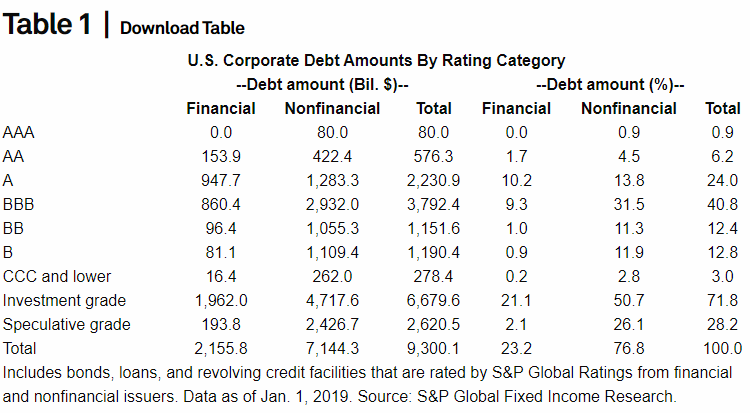

米国社債市場の規模

2019年1月のS&Pのデータによると、米国の社債総額は9.3兆ドルにのぼる。 2020年の最近では、ほぼ10兆ドルになっているようだ。

投資適格社債は7割で6.6兆ドル(S&P社の格付ではAAA〜BBBまでをinvestment grade)なのだが、投機的だと判断される社債は2.6兆ドルにものぼる。しかしながら、投資適格社債の中で一番下の格付けであるBBBでほぼジャンク級と捉えられている社債については4兆ドルにものぼるのだ。

これは新型コロナウイルス対策前の格付けであり、フォードのように新型コロナの影響を受けて格付けが下がる場合もあるため、まだ増えてくる可能性がある。

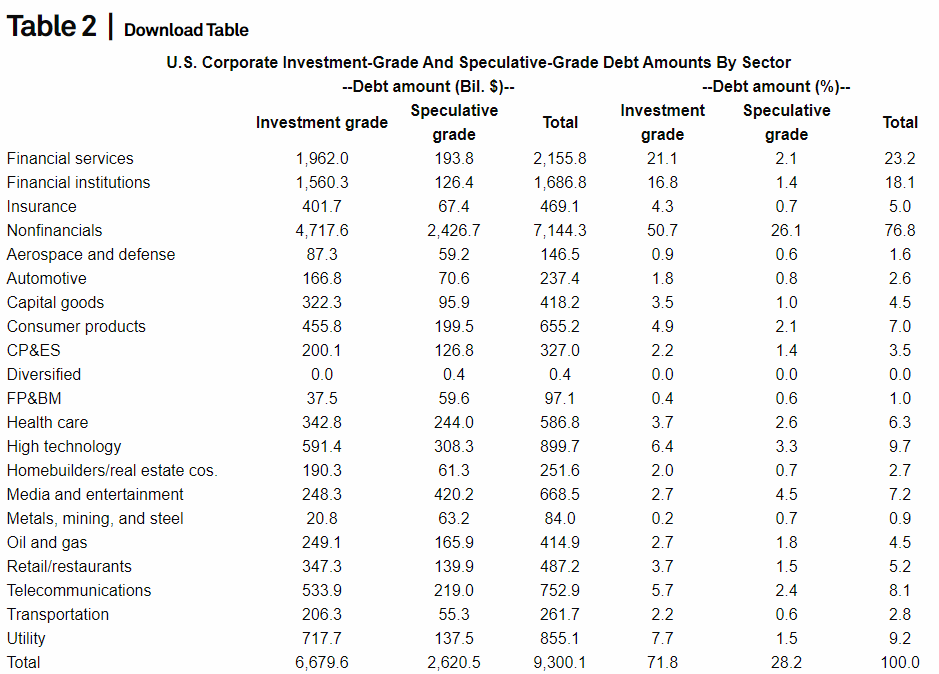

さて、次はどの業種で債券発行が多いか、投機的発行が多いかみていくことにする。懸念される石油・ガス業界の投機的社債は1659億ドルとおもったほど多くはない。ただし、投資適格級といってもBBBがどれほどあるかは明らかではない。むしろ、メディア・エンタメ、ハイテク業種は3000億ドル~4000億ドルほどあるくらいだ。これをみると、どの業種も全般的に投機的社債に該当するものが500億ドル以上はある。

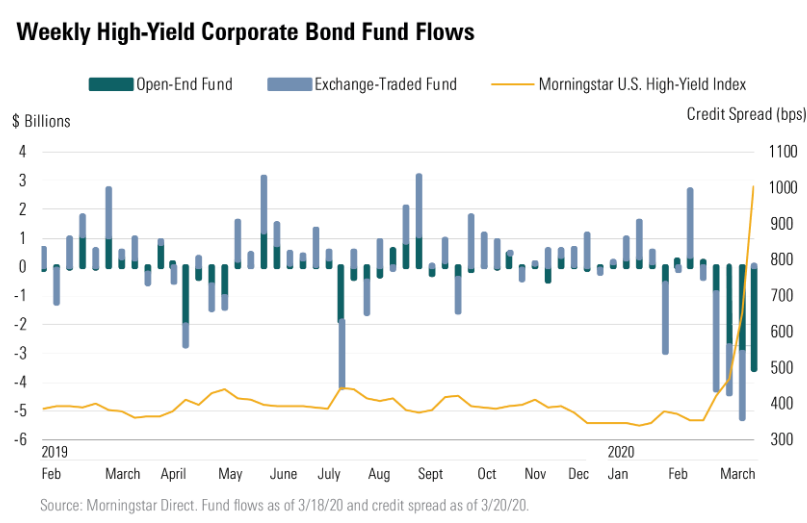

ハイ・イールド社債ファンドからの資金流出は続いている。この状況では、ハイ・イールド社債にお金が入ってこないことにもつながる。

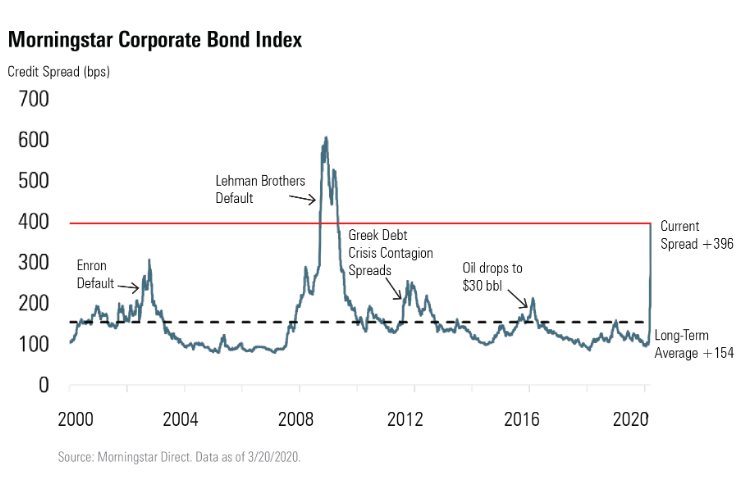

社債のクレジット・スプレッドも急上昇している。投資適格級でさえ400ポイント近くに上昇してリーマン・ブラザーズデフォルト時に近づいている。更に、ハイイールド社債については999に達していて リーマン・ブラザーズデフォルト時では1600~1800ポイントだったのでどんどん近づいている状況だ。

Over the past few weeks, credit spreads in the corporate bond markets have widened substantially. Through March 20, the average credit spread in our investment-grade index has widened out 299 basis points to +396. In our high-yield index, the average credit spread has skyrocketed 643 basis points to +999.

https://www.morningstar.com/articles/973818/corporate-bonds-at-second-widest-level-in-20-years

州政府は連邦政府の財政支援は不足していると指摘

特に感染拡大している州であるニューヨーク州、ニュージャージー州、カリフォルニア州については、政府の2750億ドルの財政支援では足りないと指摘している。なぜか見事にこれらの感染拡大地域の州政府は民主党だ。

州や群の地方債の発行は確実と思われるが、地方債の発行がどれくらいになるかまではデータが拾えていない。

The bill sets aside nearly $275 billion in emergency funds for state and local governments including $100 billion for hospitals, $45 billion in disaster relief funds, and $25 billion for transit systems, according to the Senate Appropriations Committee. There is also an expected $150 billion virus fund for states.

https://www.bloomberg.com/news/articles/2020-03-25/governors-say-massive-federal-stimulus-deal-falls-short

“We still need more federal resources directly to the states that are on the front lines of this crisis,” Maryland Governor Larry Hogan, a Republican who chairs the National Governors Association, said at a press conference Wednesday. “We’re gonna come back and ask for additional funding for the states and local governments to help with this crisis in the next round of stimulus.”

New York Governor Andrew Cuomo, whose state is the epicenter of the U.S. outbreak, slammed the deal as insufficient. New Jersey’s Governor Phil Murphy applauded the package as a positive development while acknowledging that his state with the second-highest number of cases will likely need additional aid, and Governor Gavin Newsom of California, which has the third-highest U.S. case count, said he strongly believes the federal government will need to do more. All three are Democrats.

最大4.5兆ドルもの社債や州・地方債への信用供給は大きい。しかしながら、投資適格級しか信用供給しないことや、すでに投機的社債が3兆ドルちかいこともあるので、ある程度の倒産は免れないと考えられる。新型コロナウイルス感染拡大封じ込め、あるいはロックダウンが長引けば更に痛手になるし、新たな資金調達ができなければ、倒産件数も膨れ上がるだろう。

サプライチェーンがもとに戻って供給ショックが回復しても、需要ショックはこれだけの失業者数がでたらすぐの回復は難しいと考えられる。社債崩壊はこれから訪れることになるだろう。